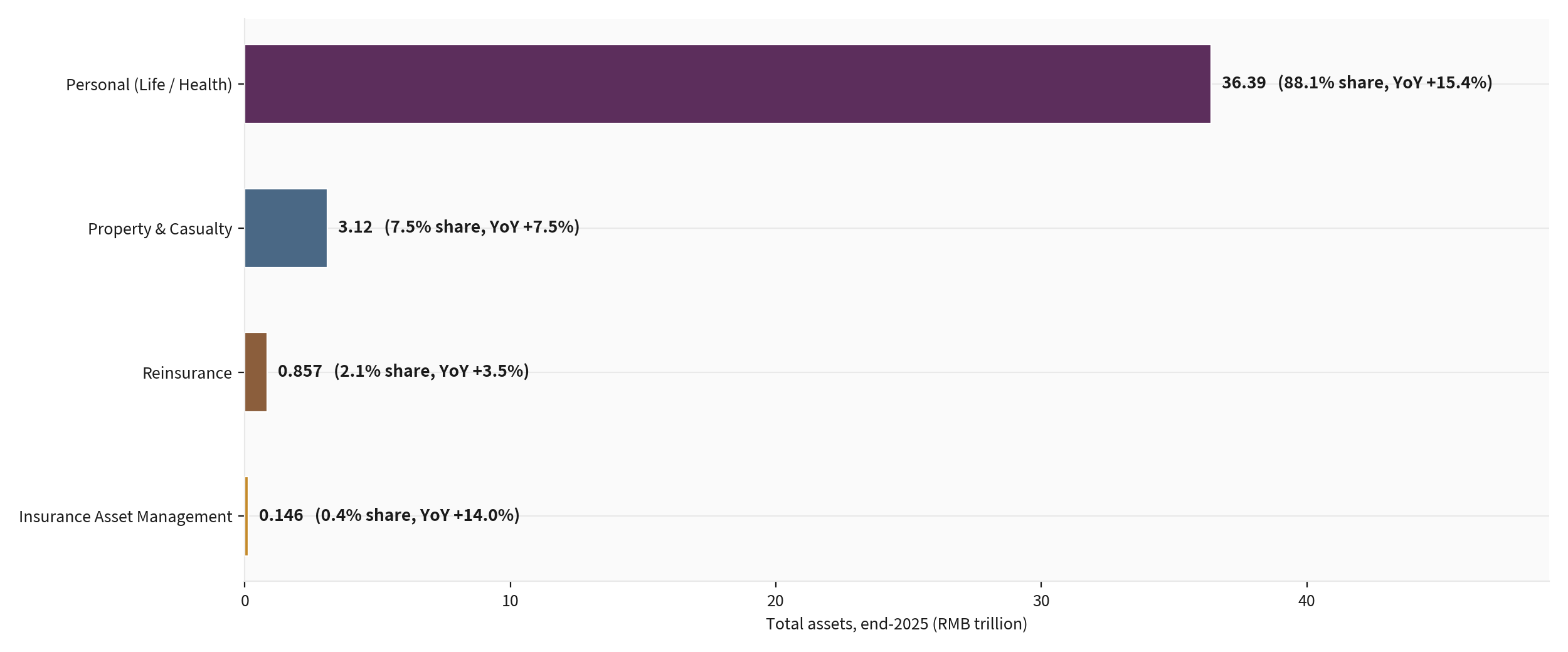

China's insurance industry: structure, premiums, and how insurers invest

China's insurance industry splits into life, property and casualty, and reinsurance, with premium income concentrated heavily in the life and health segment. How that pool of premium income gets invested, and how much solvency cushion insurers carry while investing it, shapes one of the largest sources of long-term capital in the financial system.

Industry structure and the channel shift

Life and health insurance accounts for the largest share of industry premium income, with property and casualty and a smaller reinsurance segment making up the rest. Distribution has shifted markedly over the past several years away from the individual-agent model, once the dominant sales channel, toward bancassurance partnerships with banks and increasingly toward digital and professional intermediary channels. The agent-force contraction reflects both a deliberate regulatory push toward higher-quality, better-trained distribution and a broader restructuring of how insurance products reach customers in China.

Why distribution structure matters for the rest of the industry

The channel an insurer relies on affects both the cost of acquiring a policyholder and the type of product that channel can sell effectively. Bancassurance tends to favour simpler, savings-oriented products sold alongside banking relationships, while the agent channel historically supported more complex protection products requiring face-to-face explanation. As the agent force has contracted, product mix across the industry has shifted in step, with implications for how much of the premium pool ends up in protection-style products versus savings-style products that insurers then need to invest to meet guaranteed returns.

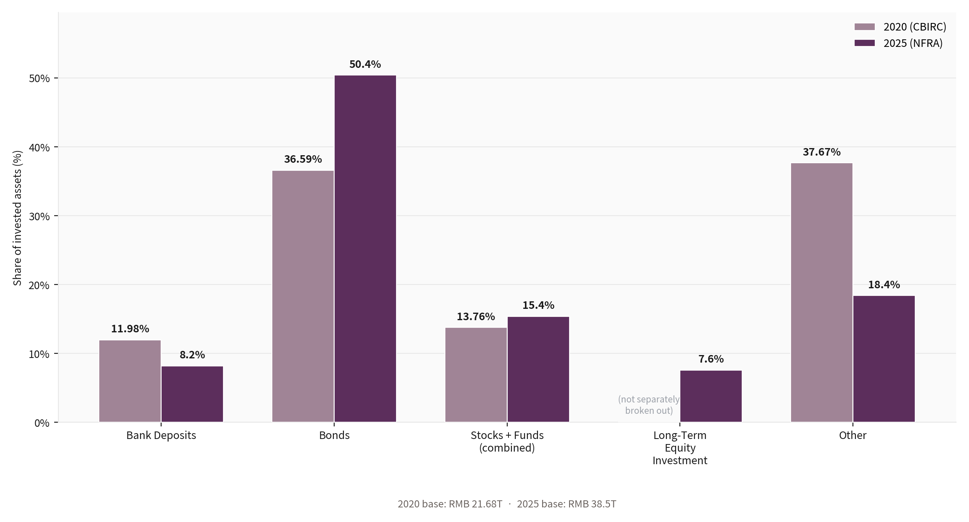

How insurers invest the premium pool

Insurance funds in China are invested across bonds, equities, and a growing allocation to alternative assets including infrastructure and real estate-related vehicles, all within limits set by the regulator. The allocation mix has shifted gradually over time toward longer-duration and somewhat higher-yielding assets, a response to sustained pressure on guaranteed product returns in a lower-rate environment. This investment behaviour makes Chinese insurers one of the more consistent sources of long-duration demand in both the domestic bond and equity markets.

Reading structure and solvency together

The two charts below show the industry's sub-sector composition and the agent-channel contraction, then the asset-allocation shift and solvency ratios by company type at end-2025. Solvency ratios, the buffer an insurer carries above the regulatory minimum, are the key check on whether the longer-duration, somewhat riskier allocation shift is being made from a position of strength or under pressure. Reading the allocation shift alongside the solvency cushion, rather than either alone, is the more complete way to judge how much capacity the industry actually has to keep extending into longer-duration assets.