China's asset management industry after the 2018 new rules

The 2018 asset-management rules reorganised China's investment industry around net-asset-value pricing and clearer regulatory perimeters, and the bank wealth-management and private-fund sectors that emerged from that reorganisation now represent two of the largest pools of managed capital in the system.

What the rules changed

Before 2018, much of China's asset-management product universe carried implicit return guarantees and allowed maturity mismatch between what a product promised investors and the actual liquidity of its underlying assets, a structure that built up hidden risk across banks, trusts, and wealth managers. The 2018 rules removed those implicit guarantees, restricted maturity mismatch, and required products to be priced and reported on a net-asset-value basis like a conventional fund, exposing investors directly to the performance of underlying assets rather than a promised fixed return.

The bank wealth-management migration

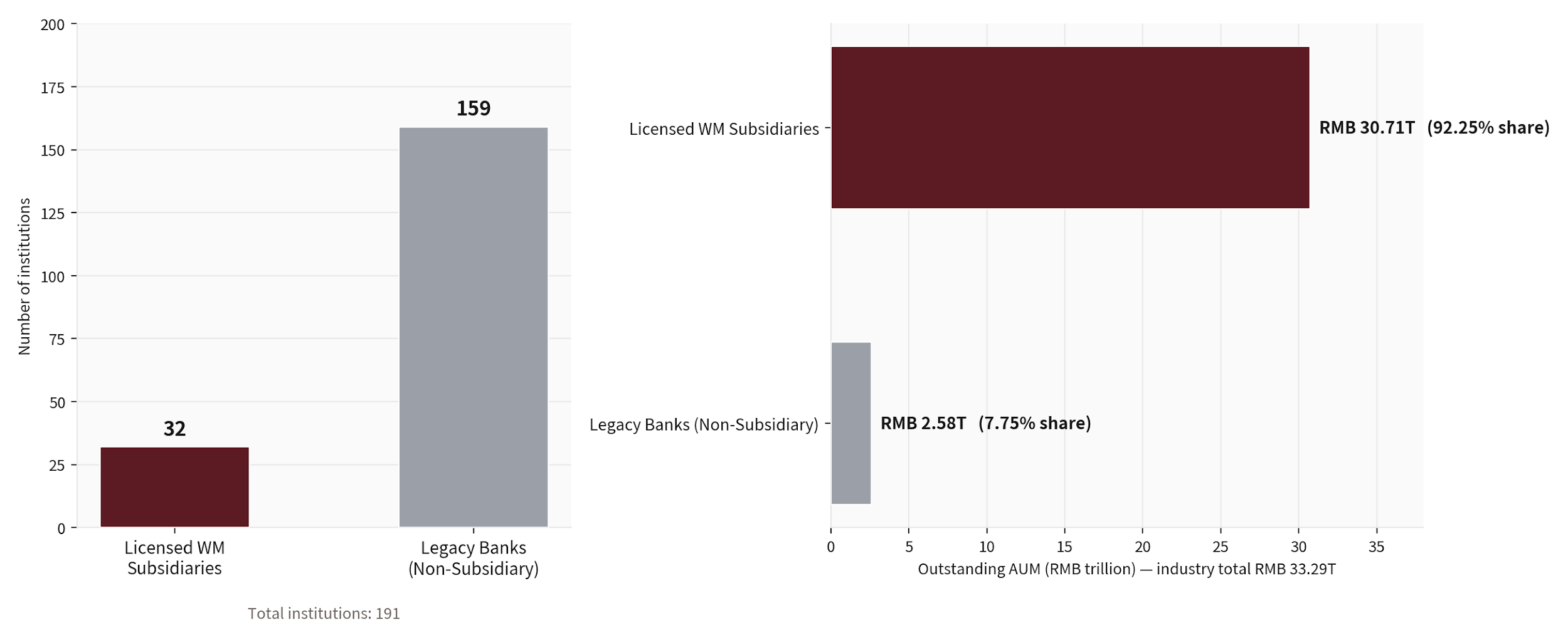

The most visible consequence was the migration of wealth-management product issuance out of banks' own balance sheets into dedicated, separately licensed wealth-management subsidiaries, a multi-year transition with a formal deadline that has now largely run its course. The split between subsidiary-issued, net-asset-value products and any remaining legacy bank-issued products is a direct measure of how far that migration has progressed at any given bank, and the industry overall has moved substantially toward the new subsidiary model.

The private-fund sector alongside it

Running in parallel, China's private-fund industry, registered with the Asset Management Association of China (AMAC), spans securities-focused funds, private equity and venture capital vehicles, and other asset-management structures. Unlike the bank wealth-management sector, private funds were not built around implicit guarantees in the first place, so the 2018 rules affected this sector less directly, though tightened registration and reporting requirements have applied across the board. The relative scale of securities, equity, and venture categories within the private-fund pool shows where professional, accredited-investor capital is currently concentrating.

Reading the post-2018 landscape

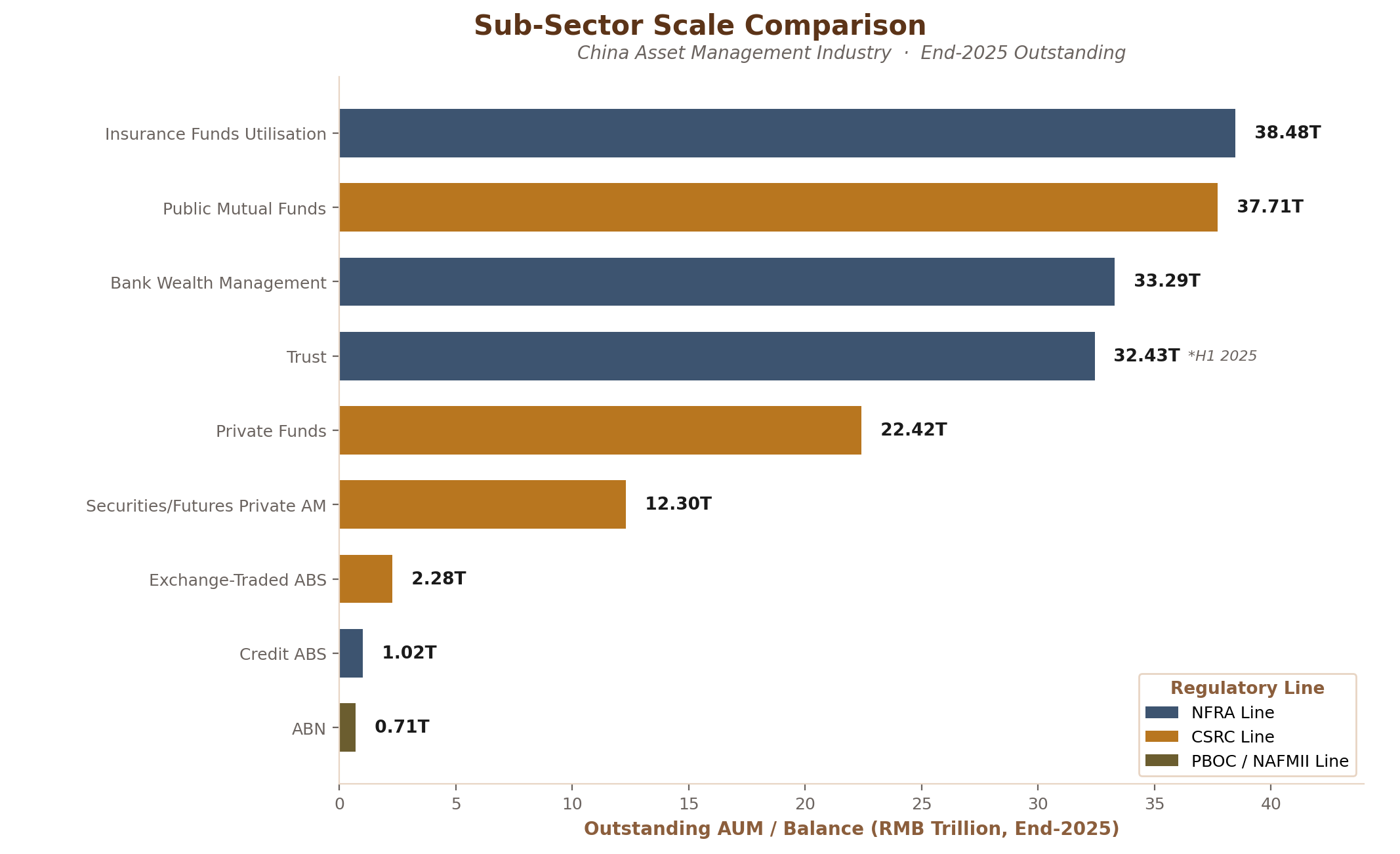

The two charts below show the broader asset-management sub-sector scale comparison, bank wealth management, insurance asset management, public and private funds, trusts, and securitisation, followed by the bank wealth-management subsidiary split and the private-fund composition specifically. Together they show an industry that has been reorganised around clearer lines without shrinking overall, with capital redistributing across sub-sectors as the old implicit-guarantee model gets replaced by transparent, NAV-based products across the board.