China's pension system and the silver economy

China's pension system rests on three pillars, a state basic pension, employer and occupational annuities, and a personal pension account now in nationwide rollout, set against a demographic backdrop that is turning aging itself into a distinct financial market, the silver economy.

The three pillars

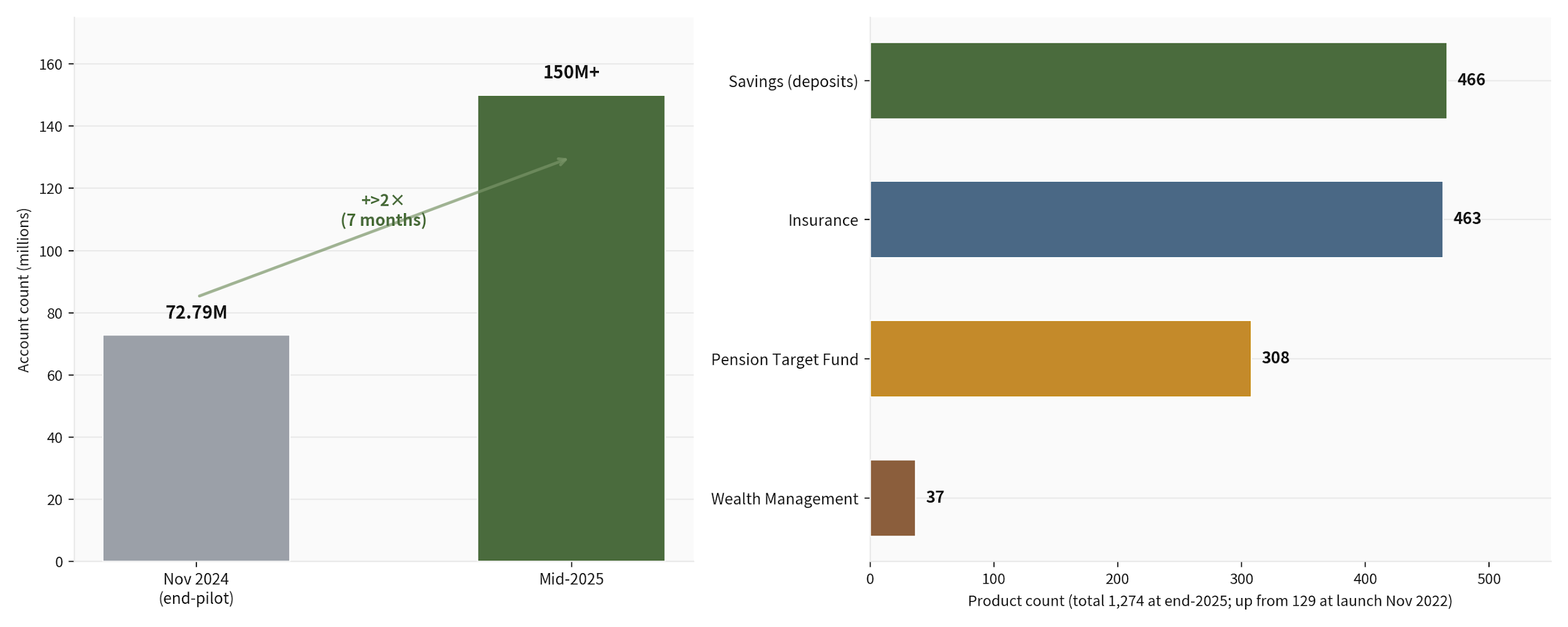

The first pillar is basic pension insurance, run by the state and covering the large majority of the working population through mandatory contributions. The second pillar covers enterprise and occupational annuities, funded jointly by employers and employees on a voluntary basis and concentrated more heavily among larger employers and state-owned enterprises. The third pillar, the personal pension account, is a tax-advantaged individual savings wrapper that moved from a pilot programme in 36 cities to full nationwide availability, holding a defined menu of eligible mutual funds, commercial pension insurance products, bank wealth-management products, and savings deposits.

Why the third pillar is the growth story

With the first pillar carrying the great majority of retirement income provision and facing a rising dependency ratio as the population ages, policy has pushed deliberately toward private accumulation through the third pillar to relieve pressure on the state system over time. The annual contribution ceiling, tax treatment at contribution and withdrawal, and the expanding menu of eligible products are all levers regulators have used to encourage uptake since the national rollout, and participation and account growth are the clearest read on whether that policy push is translating into actual behaviour change among savers.

The silver economy as a market

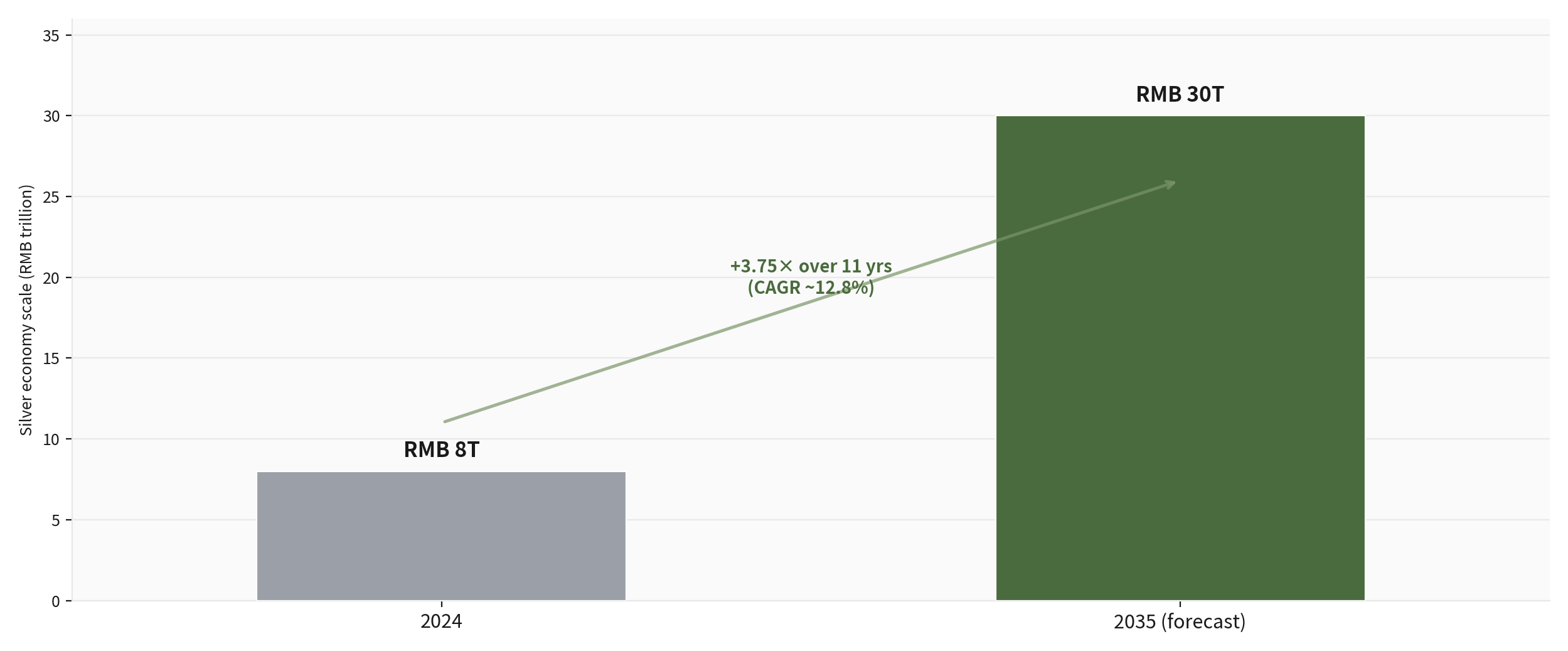

Stepping back from pension policy specifically, the same demographic shift, a rising share of the population aged 60 and over, is giving rise to a broader silver economy spanning eldercare services, healthcare finance, age-appropriate housing, and insurance products tailored to longer life expectancy. Long-term care insurance, in particular, has moved from scattered city-level pilots toward a more structured national framework, reflecting the same underlying demand the pension system is responding to from a different angle: how to finance a longer retirement for a larger share of the population.

Reading pension growth against the demographic curve

The two charts below show personal pension account growth and the widening product menu, then the silver-economy trajectory toward 2035 against the underlying demographic structure. The connection between them is direct: every year the dependency ratio rises is a year of added urgency behind third-pillar uptake and silver-economy build-out alike. Reading pension account growth in isolation, without the demographic chart alongside it, understates how much catching up the system still has to do relative to the pace of the underlying aging curve.