RMB internationalisation: payments, e-CNY, and the cross-border rails

The RMB's progress toward becoming a more widely used international currency runs on two tracks at once: its share of global payments messaging, and the physical and digital rails, CIPS, the digital RMB, and the multilateral mBridge platform, that move it across borders. Neither track tells the full story alone.

The payments share as a transactional signal

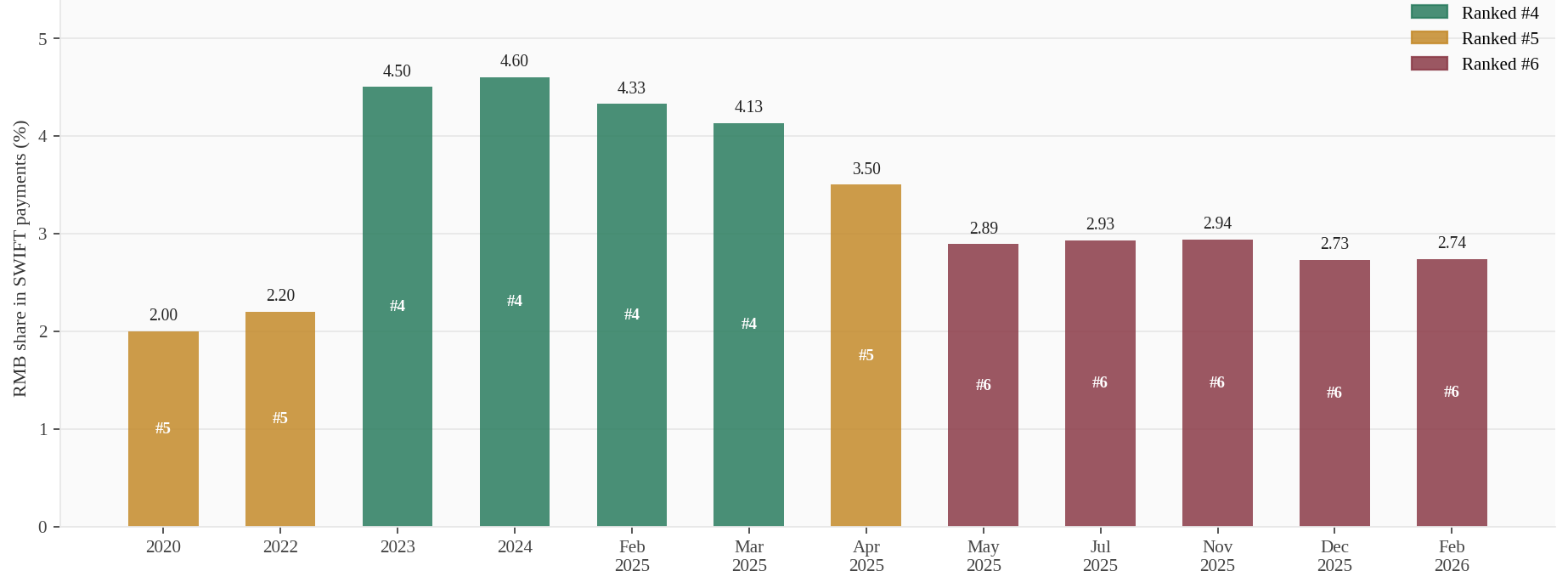

The cleanest single read on RMB internationalisation is its share of value in global payments messaging, tracked monthly by SWIFT's RMB Tracker, alongside the currency's ranking against the dollar, euro, and other major currencies. That share moves with trade settlement volumes, offshore RMB liquidity conditions, and seasonal patterns, so a single month's swing carries less signal than the direction over several quarters. The ranking is a useful shorthand for where the RMB sits in the global pecking order, but the underlying share number is the figure worth tracking closely, since rankings can shift on small changes near a threshold.

The three rails that carry it

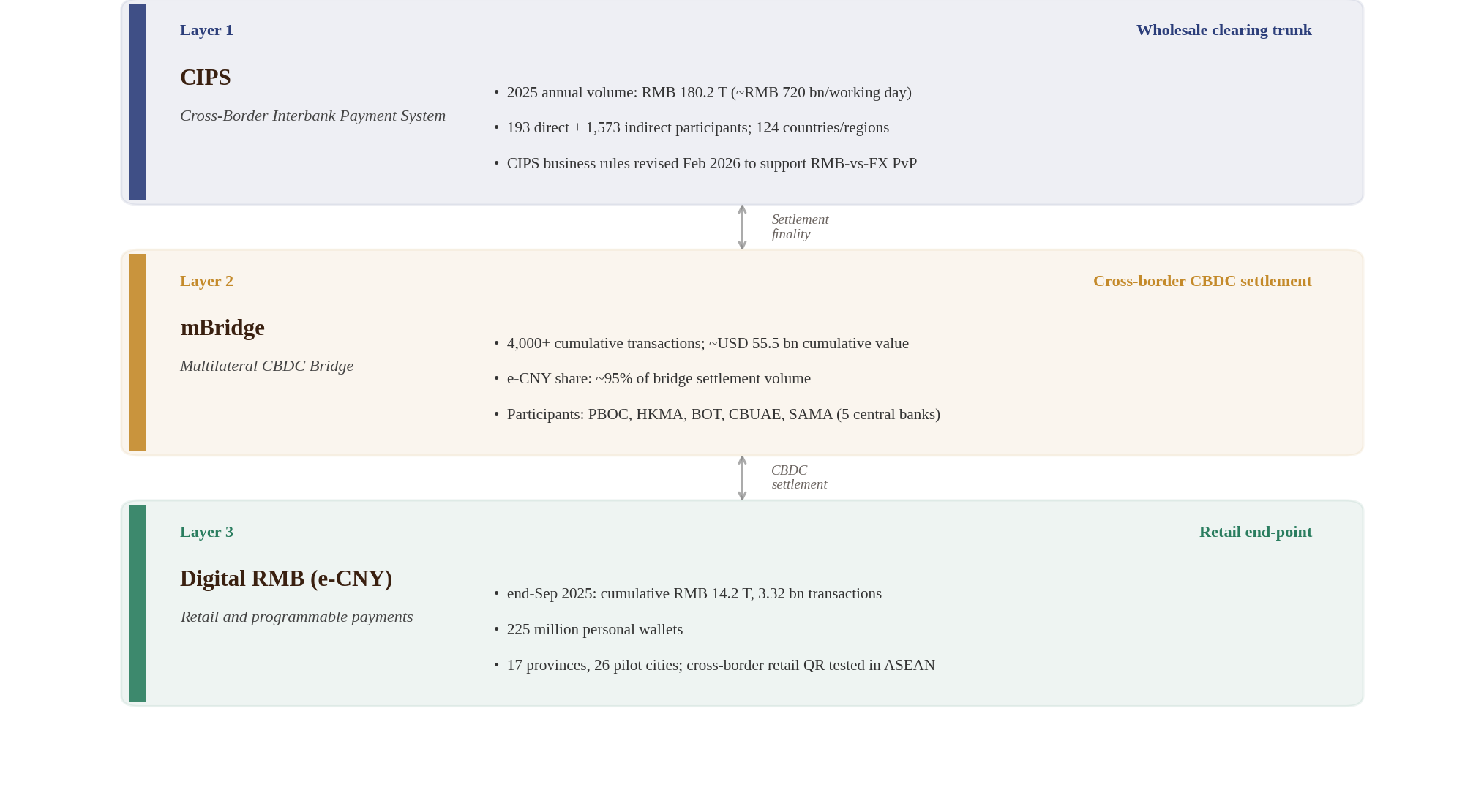

Behind the payments share sit the actual settlement rails. The Cross-Border Interbank Payment System, or CIPS, clears RMB payments between participating banks and is the backbone equivalent to what SWIFT does for messaging, though CIPS handles settlement rather than messaging alone. The digital RMB, or e-CNY, started as a domestic retail token and has since been extended into selected wholesale and cross-border pilot programmes. The third rail, mBridge, is a multilateral platform built jointly by several central banks, including the Digital Currency Institute of the People's Bank of China, to settle central bank digital currencies directly between participating jurisdictions without routing through a correspondent bank chain.

Why the rails matter independently of the payments number

A currency's payments share can rise even without infrastructure investment, simply through trade growth. The rails matter because they determine how much friction sits in the system long-term, and because governance of those rails has been shifting. Project mBridge moved from a Bank for International Settlements-incubated pilot to direct ownership by its founding central banks in 2024, when the BIS Innovation Hub stepped back from day-to-day involvement, a structural change in who controls the platform's future direction. CIPS, by contrast, has expanded its participant network steadily without a comparable governance shift, since it sits squarely under PBOC's own clearing infrastructure.

Reading payments share and rails as one picture

The two charts below put the CIPS, e-CNY, and mBridge architecture next to the SWIFT payments share and currency ranking. Together they answer a question neither answers alone: is RMB use growing because more capacity exists to move it, or because trade and liquidity conditions are pushing more transactions through existing rails regardless of capacity. Watching both side by side, rather than picking whichever one is moving in a given quarter, is the more reliable way to track where RMB internationalisation actually stands.