China's cross-border investment channels: QFII, Connect, and the RMB dashboard

Capital moves into and out of China through a defined set of named channels rather than a single open capital account. Reading those channels alongside a broader RMB internationalisation dashboard shows how managed opening and currency use are advancing together, on related but separate timelines.

The channel architecture

Foreign access to Chinese securities runs through several parallel routes: the Qualified Foreign Institutional Investor (QFII) and RMB Qualified Foreign Institutional Investor (RQFII) schemes, which grant licensed access to onshore securities; Stock Connect and Bond Connect, mutual-market links settled through Hong Kong without a separate onshore account; and a wealth-management connect scheme covering products in the Guangdong-Hong Kong-Macao Greater Bay Area. Each channel carries its own eligibility rules, quota structure where applicable, and settlement mechanics, and the State Administration of Foreign Exchange (SAFE) oversees the foreign-exchange dimension of all of them under China's broader managed capital-account framework.

Why multiple channels rather than one

Running several channels in parallel, rather than a single unified gateway, lets regulators calibrate access by investor type and asset class without reopening the whole capital account at once. A large global custodian bank might use QFII for direct onshore bond exposure while routing equity exposure through Stock Connect, depending on which channel offers better settlement terms for that asset class. This layered structure is also why cross-border investment data needs to be read channel by channel rather than as one aggregate flow number, since each channel responds to different policy levers and different investor bases.

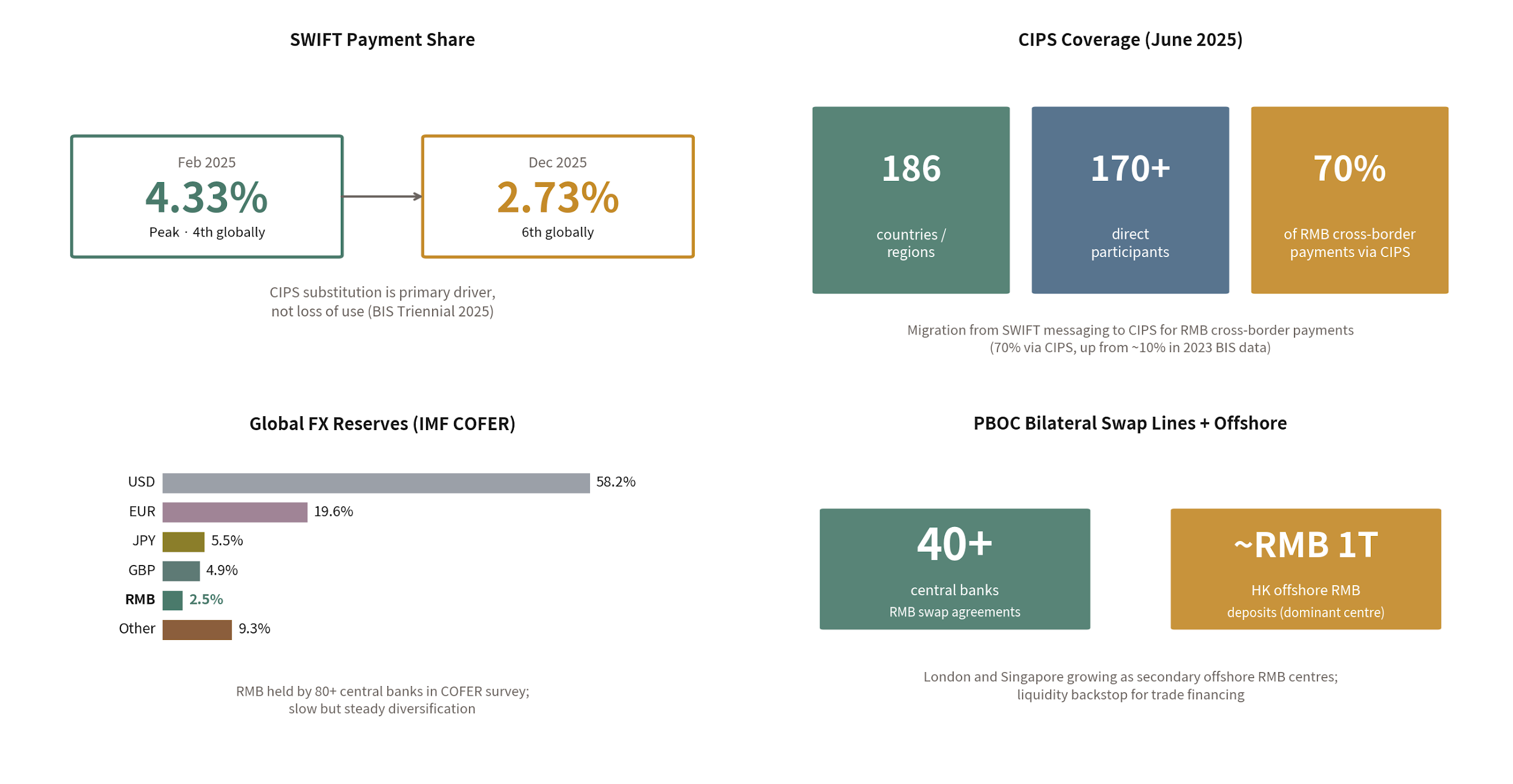

The RMB dashboard view

Stepping back from individual channels, a broader RMB internationalisation dashboard tracks several metrics side by side: payments share, trade settlement in RMB, RMB holdings in global reserves, and offshore RMB deposit pools in centres like Hong Kong and Singapore. No single metric on this dashboard moves in lockstep with the others. Reserve holdings shift slowly, tied to central bank allocation decisions; offshore deposits respond faster to interest-rate differentials and capital controls; trade settlement tracks the underlying flow of goods. Reading the dashboard as a whole, rather than any one line, gives the more reliable signal of direction.

Channels and dashboard together

The two figures below set the seven-channel investment architecture next to the multi-metric RMB dashboard for 2025. The connection between them is direct: every channel that widens foreign access to onshore RMB assets is also, mechanically, a contributor to several lines on the dashboard, particularly offshore holdings and cross-border settlement volume. Watching channel-level policy announcements, a new connect scheme, an expanded quota, a relaxed eligibility rule, is one of the more reliable leading indicators for where the broader RMB metrics are likely to move in the following quarters.