How the PBOC runs monetary policy: rates, reserves, and the Loan Prime Rate

The People's Bank of China, or PBOC, manages liquidity and the cost of credit through a small set of interlocking tools: the money supply, the reserve requirement ratio banks must hold against deposits, a short-term rate corridor, and a benchmark lending rate that carries policy into the real economy. Understanding how these fit together explains most of what moves Chinese short rates.

The quantity side: M2 and the reserve requirement

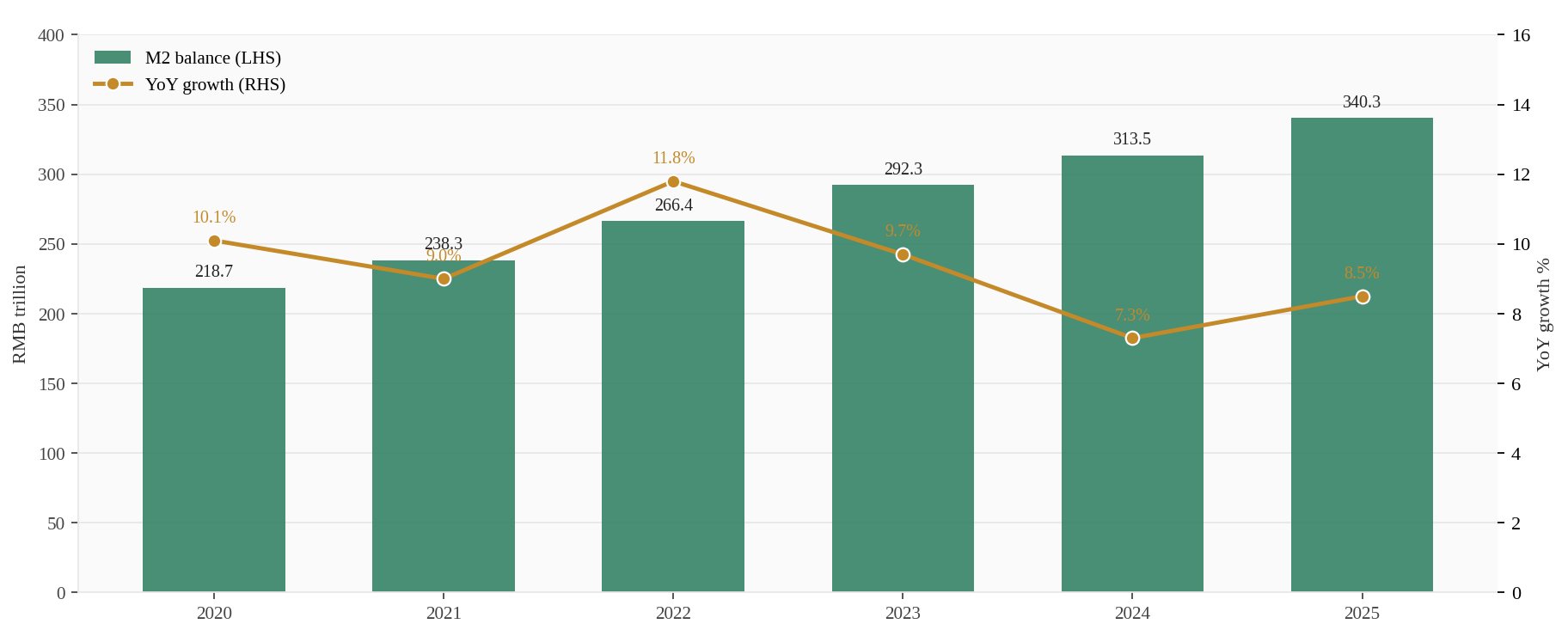

Broad money supply, M2, is the headline quantity gauge, tracking how much money and near-money sits in the banking system. The PBOC influences that quantity directly through the weighted-average reserve requirement ratio (RRR), the share of deposits banks must hold back rather than lend out. Cutting the RRR frees reserves for lending without the central bank creating new base money outright, which is why RRR cuts function as a quieter, more targeted lever than outright rate cuts. The M2 growth rate, read against nominal GDP growth, is one of the simplest checks on whether credit conditions are loosening or tightening relative to the size of the economy.

The price side: the rate corridor

Sitting above the quantity tools is a price-based corridor. The PBOC sets a ceiling and floor for short-term money market rates using standing lending and deposit facilities, with open market operations and the medium-term lending facility doing the work of keeping actual rates inside that band. This corridor approach, common among major central banks, lets the PBOC manage day-to-day liquidity without constant manual intervention. Where short rates sit inside the corridor at any point signals whether the central bank is leaning toward easier or tighter conditions, ahead of any formal rate announcement.

Where it all lands: the Loan Prime Rate

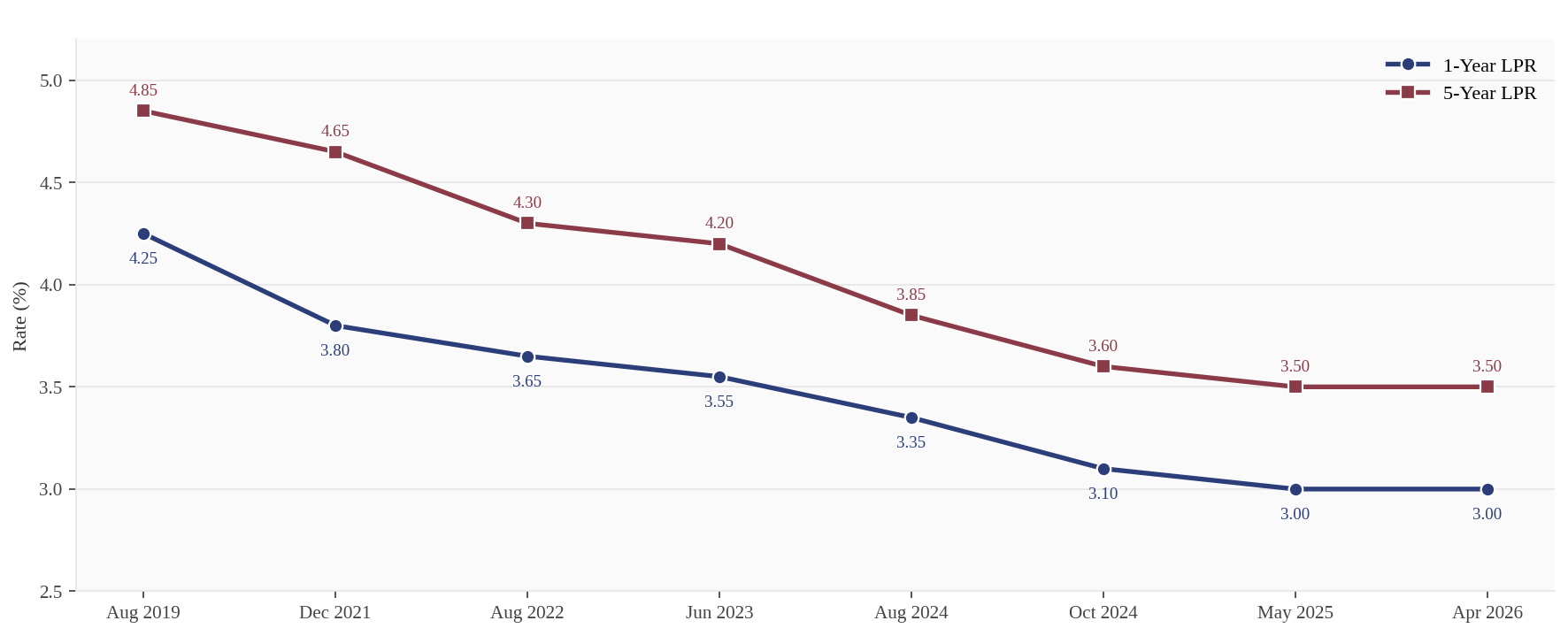

The corridor's influence reaches borrowers through the Loan Prime Rate, or LPR. A panel of quoting banks submits rates referenced off the central bank's policy rate, and the PBOC publishes a 1-year LPR, which anchors most corporate lending, and a 5-year LPR, which anchors mortgage pricing. When the policy rate moves, the LPR is the transmission channel that carries that move into what a company or a homebuyer actually pays. The chart below sets the M2 and RRR path against the LPR and corridor levels, making the full chain, from quantity tool to price tool to borrower-facing rate, visible on one timeline.

Why the chain matters more than any single print

Financial media tends to cover each of these in isolation, an RRR cut here, an LPR move there, as standalone news events. They are not standalone. An RRR cut without a corresponding move in the corridor is a liquidity gesture; an LPR cut without supporting quantity easing risks squeezing bank margins, since LPR sets what banks earn on loans while funding costs move separately. Reading the three together, quantity, corridor, and LPR, is the difference between reacting to a single headline and understanding the actual stance of policy at a given point in the cycle.