The Hormuz Switch: What the US-Iran Oil Trade Is Actually Pricing

Markets have priced the negotiation as a binary on-off switch. The logic behind that framing, and the question of who pays for it, tells you more than the day's price on a barrel.

One switch, on or off

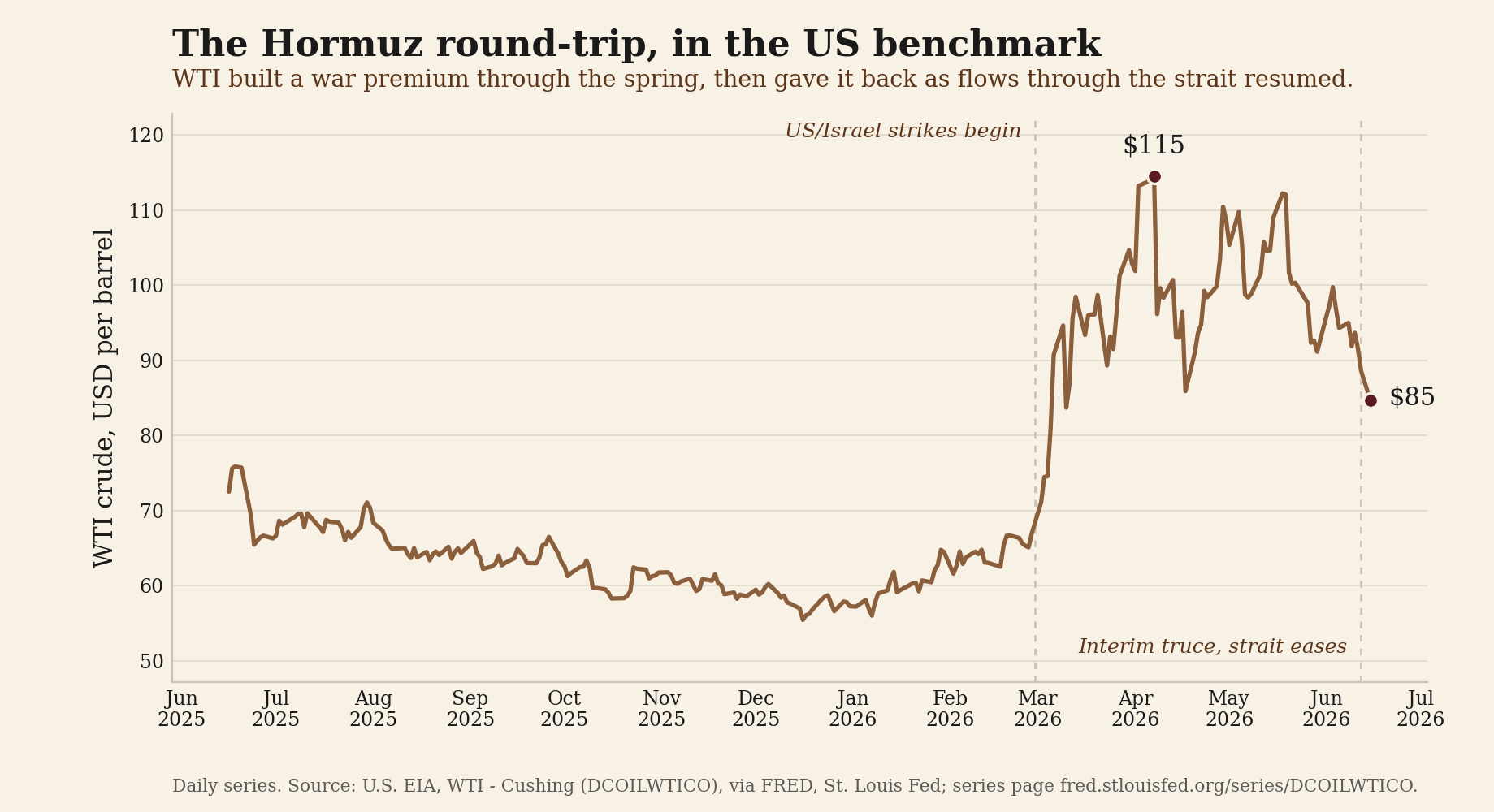

Since the American and Israeli strikes on Iran began on February 28, the oil market has read the whole negotiation through one question: is the Strait of Hormuz open or shut. The war premium went on fast. When an interim understanding took hold this month and traffic through the strait began to ease, it came off almost as fast, even as a planned round of talks in Switzerland collapsed. That round-trip is the tell. The barrel priced access to a passage. Reserves and production schedules were beside the point.

Insurance on a chokepoint

Hold onto that distinction, because it organizes everything else. Around a fifth of the world's seaborne crude moves through Hormuz, and since oil is fungible and clears at one global margin, the state of that one waterway can set the price of barrels that go nowhere near it. The premium is really insurance on a chokepoint, loosely tied to the supply it stands in for. Treat the move as an ordinary supply-and-demand story and you miss what the market is doing, which is quoting the odds on a gate.

From lever to toll

Tehran has been trying to turn that gate into a fee. During the fighting it floated mandatory insurance on ships transiting the strait, free at first and billable later, and its parliament drafted legislation to charge for passage. The shift in kind matters more than the numbers. An open-or-shut event, waited out once, becomes a standing claim on each cargo that crosses, and that is a different object for a market to hold. One is a spike. The other is a toll, priced for as long as the lever exists.

Who actually pays

The sharper lens is incidence: who actually pays for a contested strait. Two seats sit at the table, Washington and Tehran, yet the cost lands downstream, on the importers who buy what flows through, and that demand sits mostly in Asia. It arrives through the currencies of energy importers and through the share prices of the refiners, shippers, and manufacturers that run on imported feedstock. China, a principal buyer of Gulf crude, carries that exposure while holding no chair in the room.

No exemption at the margin

The same mechanism explains why a strait that almost no American barrel crosses still turns up at an American pump. Pumping your own oil buys no exemption once you price at the global margin. US refiners pay the world price, the domestic benchmark follows the international one through arbitrage, and because crude trades in dollars the cost lands with no currency cushion to soften it. You could see it in the May inflation figures, where energy supplied the bulk of a fresh pickup in headline prices, as the Bureau of Labor Statistics tallied it, while the core measure held near target, and in the Federal Reserve's answer: a hold at the June meeting alongside projections that turned hawkish, a central bank treating a supply shock it cannot offset as a risk it cannot look past.

Two clocks

The talks themselves have started to break along the same line. Iran has signaled it would split the files, reopening the strait and pausing the war while it defers the nuclear question, according to reporting by Axios. Markets read the separation as constructive, for a structural reason. Hormuz is the fast variable, marked to market each day in the tanker count. The nuclear file is the slow one, measured in enrichment stocks and inspection access. Pricing the two on one clock had overstated how quickly the second could move.

Spot relief, structural overhang

What remains is spot relief resting on a structural problem. The European powers triggered the JCPOA snapback in August 2025, putting prior UN sanctions back in force; Iran's parliament has suspended cooperation with the IAEA; and the cancelled Switzerland round shows how thin the current calm runs. For anyone positioning around the talks, the right gauges follow from the framing rather than the headline price. Watch tanker traffic through Hormuz for whether the truce holds, the insurance-and-fee proposal for whether a lever is hardening into a toll, and the nuclear track for whether the decoupling that settled the oil curve survives the harder file. The barrel will keep moving first. The question worth asking is what it is voting on, and who is being asked to honor the vote.