China's GDP and demographics in 2025: the numbers that frame every market

Two long series sit behind every call on Chinese markets: the growth path of the economy and the aging curve of its population. Neither moves quickly, and together they set the backdrop against which every shorter-term policy decision gets read.

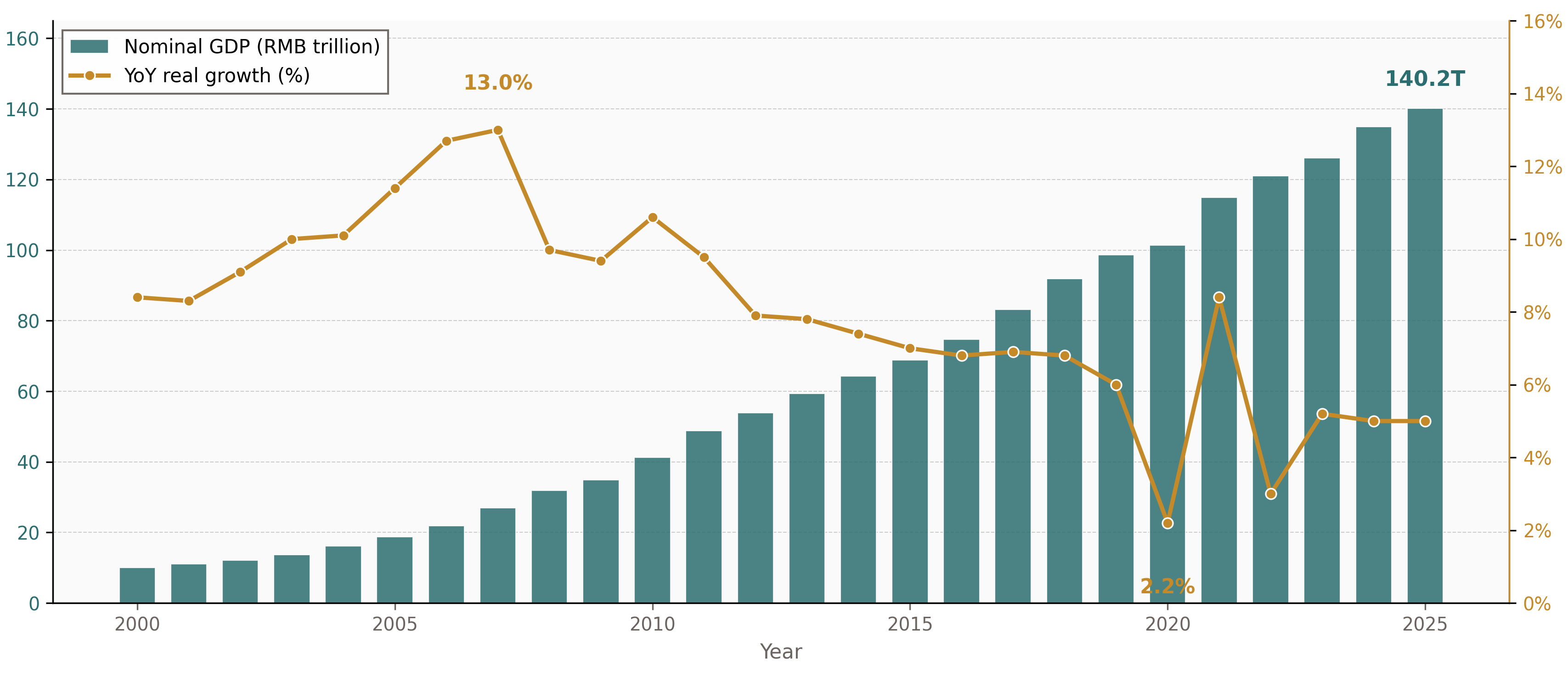

A slower, services-weighted economy

China's real growth rate has settled onto a lower plateau than the double-digit decades of the 2000s, as the economy shifts weight from investment and export-led manufacturing toward services and higher-value output. This is a structural transition rather than a single-year event, and the official statistical record tracks it through national accounts published quarterly. Reading the GDP print in isolation misses the point. The level matters less than the composition: which sectors are carrying growth, and whether the rate is being delivered by credit expansion or by productivity.

The demographic clock underneath

Running parallel to the growth story is a demographic one that moves on a much longer clock. The share of the population aged 60 and over, and the narrower band aged 65 and over, has risen steadily as China's working-age cohort peaked and began to contract. This shift tightens labour supply over time, raises the dependency ratio, and lifts demand for pensions, healthcare finance, and long-term savings products. It is an accounting identity already locked in by birth cohorts from decades past, which is part of why it carries more certainty than most macro variables.

Reading the two series together

The chart below sets the growth path against the aging trajectory on the same timeline. The value of viewing them together is that they pull policy in different directions at once: a slower growth rate raises the urgency of pension and healthcare financing just as the population needing that financing is growing as a share of the whole. Comparing China's trajectory with other economies in the region adds context. Japan moved through a similar aging transition a generation earlier, at a higher income level; India sits at the opposite end of the demographic curve, with a still-expanding working-age population.

Why this pairing matters beyond China

For anyone pricing Chinese assets or reading policy signals out of Beijing, this pairing is the starting frame. A monetary easing cycle reads differently against a backdrop of structurally slower growth than against a cyclical dip. A push toward the personal pension system, covered elsewhere on this desk, reads differently once the dependency math is visible. Treat the growth rate and the demographic share as a matched pair rather than two unrelated indicators, and the rest of China's financial architecture, from bond issuance to insurance product design, starts to make more sense as a response to this fixed backdrop rather than a series of disconnected policy moves.