How China resolves financial risk: property, local debt, and shadow banking

China's approach to financial risk runs through three connected fronts at once, property-sector stress, local-government financing-vehicle debt, and shadow-banking exposures, each handled through its own dedicated workout channel but governed by the same stated set of resolution principles.

Three fronts, one playbook

Property-sector stress centres on developer balance sheets and the pre-sale financing model that left many projects unfinished when financing tightened. Local-government financing vehicle (LGFV) debt reflects years of off-budget infrastructure borrowing by local governments through special-purpose entities, debt that stays off formal government balance sheets while carrying implicit local-government backing. Shadow-banking exposures, concentrated in trust products and wealth-management vehicles that sat outside standard bank lending channels, layer on top of both. Each front has its own dedicated regulatory workout mechanism, but all three are handled under a consistent, publicly stated approach rather than improvised case by case.

The stated resolution principles

Policymakers have repeatedly articulated a set of resolution principles that apply across all three fronts: contain spillover before it spreads to systemically important institutions, allocate losses to the parties closest to the risk rather than socialising them broadly, and stabilise funding conditions for the broader system while individual workouts proceed. In practice, this has meant a sequence of measures including project-level guarantee mechanisms for unfinished housing, special bond programmes for local governments to swap out higher-cost LGFV debt, and tightened rules on trust and wealth-management product structuring to reduce future shadow-banking buildup.

Why sequencing, not speed, is the design

The resolution approach across all three fronts favours managed, sequenced workouts over rapid, comprehensive resolution, reflecting a judgment that uncontrolled deleveraging carries more systemic risk than a slower, monitored unwind. This sequencing is itself a signal worth tracking: an acceleration in special bond issuance for local-government debt swaps, for instance, indicates the resolution timetable on that front is being compressed, while continued incremental measures on property suggest the slower pace is judged still manageable.

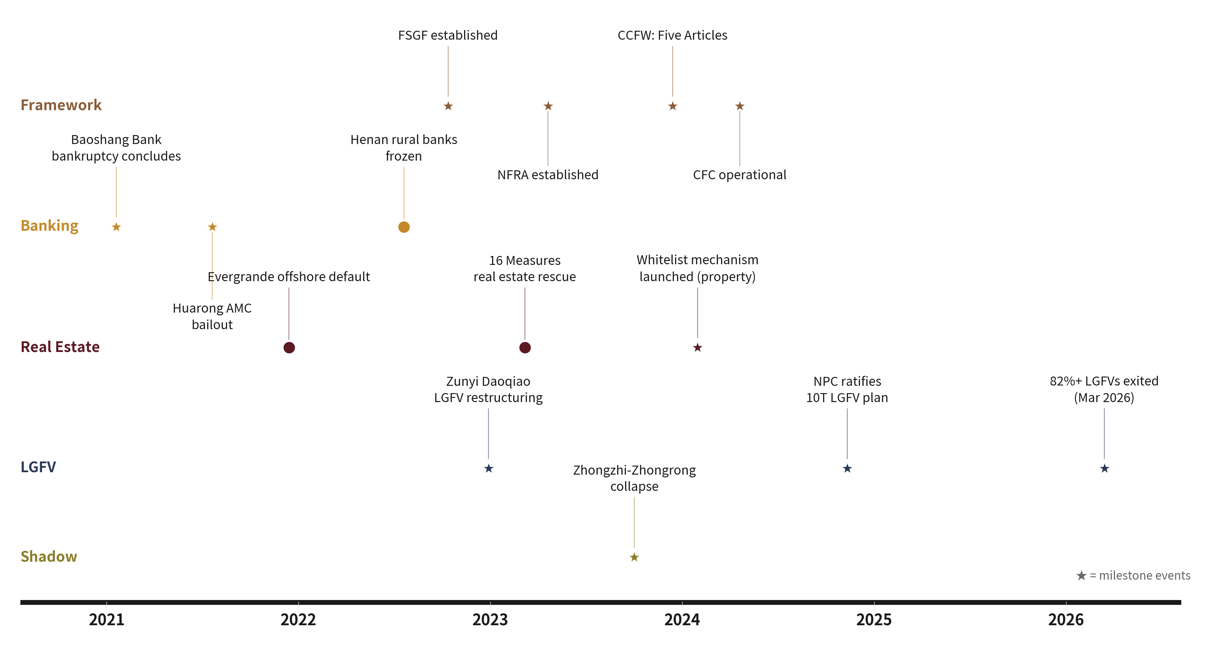

Reading the timeline

The chart below maps major risk events and resolution measures from 2021 through 2025 against the four stated resolution principles. The value of the timeline view is in seeing which front is moving fastest at any given point and which measures on each front are being repeated or escalated, a more useful signal for assessing risk trajectory than any single event taken on its own.