China's A-share IPO market: counts, proceeds, and the 2025 reset

The pace of new listings on China's A-share market is set less by company demand to go public than by the regulator's calibration of approvals under the registration-based listing system. 2025 marked a reset in that pacing, visible in both the count of new listings and the capital they raised.

From approval-based to registration-based

China completed the shift to a registration-based IPO system in 2023, moving the substantive review of listing applications from the China Securities Regulatory Commission (CSRC) to the exchanges themselves, with the CSRC retaining oversight and final registration authority. The change was meant to speed up listings and let market forces play a larger role in IPO pricing. In practice, the regulator has continued to manage the overall pace of new issuance closely, treating IPO volume as a lever connected to broader market stability rather than a purely demand-driven pipeline.

Why pacing, not just rules, drives the count

The count of new listings and the proceeds they raise in any given year reflect this pacing as much as they reflect underlying corporate demand to access public markets. In periods when secondary-market sentiment is fragile, the regulator has slowed approvals to avoid adding supply into a weak market, a pattern that has repeated across several cycles. In stronger periods, the pipeline opens up again. This is a deliberate stability tool rather than an oversight gap, and it means IPO volume is one of the more direct readable signals of how the regulator is weighing growth support against market stability at any given time.

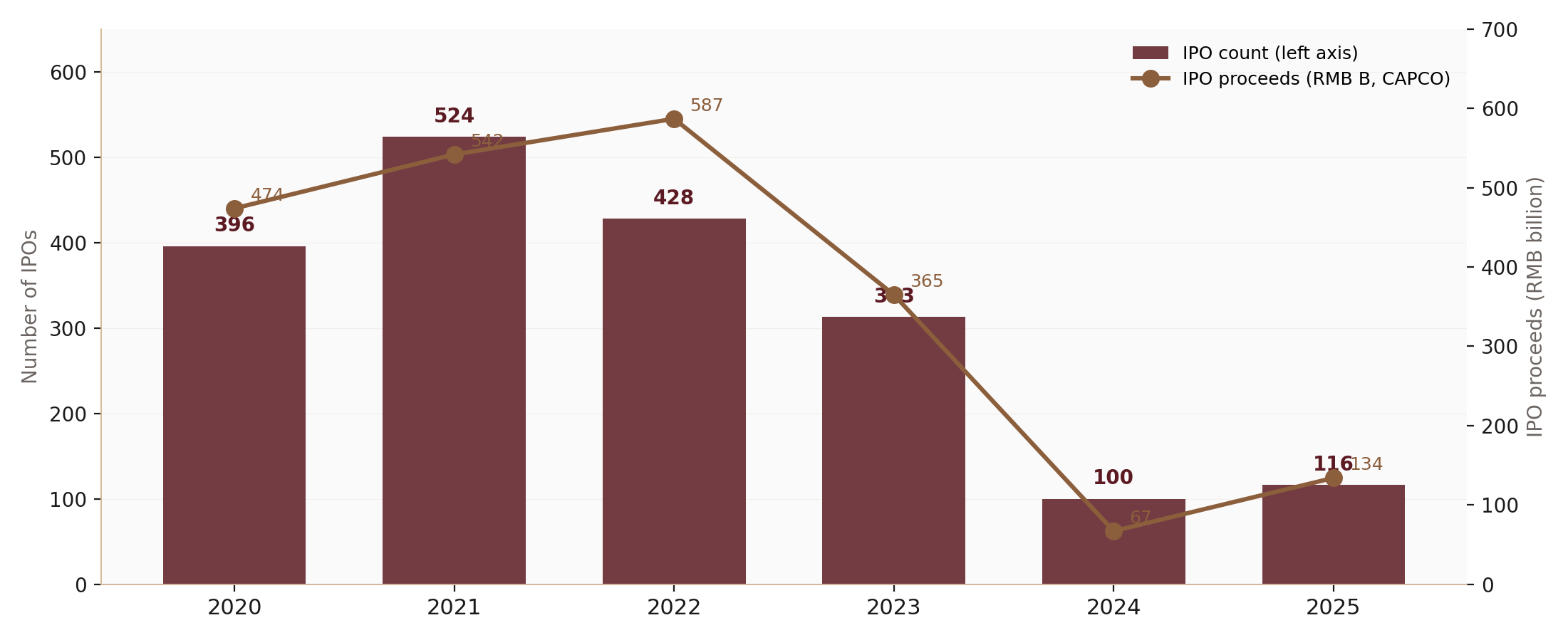

What the 2025 reset looked like

The chart below shows IPO counts and proceeds raised from 2020 through 2025. The pattern across those years is one of pacing that tightens and loosens with broader market conditions rather than a steady upward trend, consistent with a managed rather than fully market-driven listing pipeline. Reading the count alongside proceeds matters: a year with many small listings and modest proceeds tells a different story about market depth than a year with fewer, larger listings raising similar aggregate capital.

Beyond IPOs: the full equity-capital picture

New listings are only one channel for raising equity capital. Refinancing by already-listed companies, through follow-on offerings and convertible issuance, and dividend payouts back to shareholders complete the broader picture of how capital moves through China's listed equity market. A full read of equity-capital formation in any given year needs all three pieces, new listings, refinancing, and distributions, since regulators have at times tightened one channel while leaving others untouched, shifting where companies turn to raise money without necessarily reducing overall equity-capital activity.