AI and platform finance in China: adoption, rectification, and the new normal

Two technology-driven shifts have reshaped Chinese financial services in recent years: the uneven rollout of AI across different financial functions, and the rectification of large technology platforms' financial arms, which has given way to an ongoing, rules-based framework rather than one-off enforcement action.

Where AI adoption actually stands

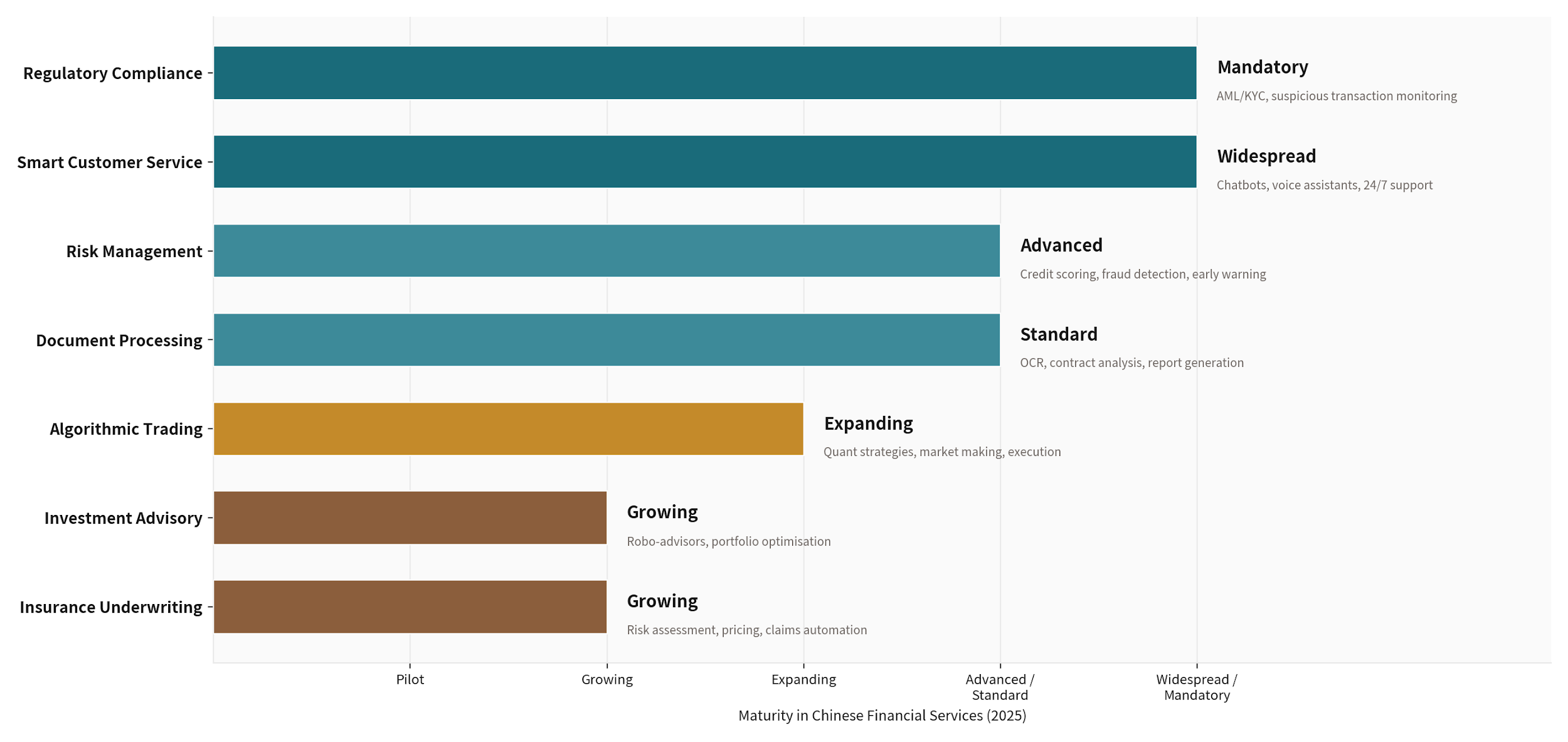

Adoption of AI tools across Chinese financial services is uneven by function rather than uniformly advanced or uniformly early. Customer service, fraud and risk screening, and document processing show the most mature deployment, reflecting high-volume, pattern-heavy tasks where models slot into existing workflows with relatively contained downside if they make an error. Investment research, portfolio construction, and regulated financial advice sit earlier on the adoption curve, held back by data-governance requirements, model-risk management rules, and the simple fact that errors in these functions carry a higher and more direct cost to end customers.

From platform rectification to standing framework

The campaign that reset the financial arms of large technology platforms, addressing concerns about data concentration, unlicensed lending activity, and systemic risk building up outside the regulated banking perimeter, has given way to an ongoing, rules-based supervisory framework rather than continued one-off enforcement actions. Platforms that survived rectification now generally operate under licensing structures closer to those of traditional financial institutions, with capital and data-governance requirements that did not previously apply to their financial activities.

The policy framework tying both together

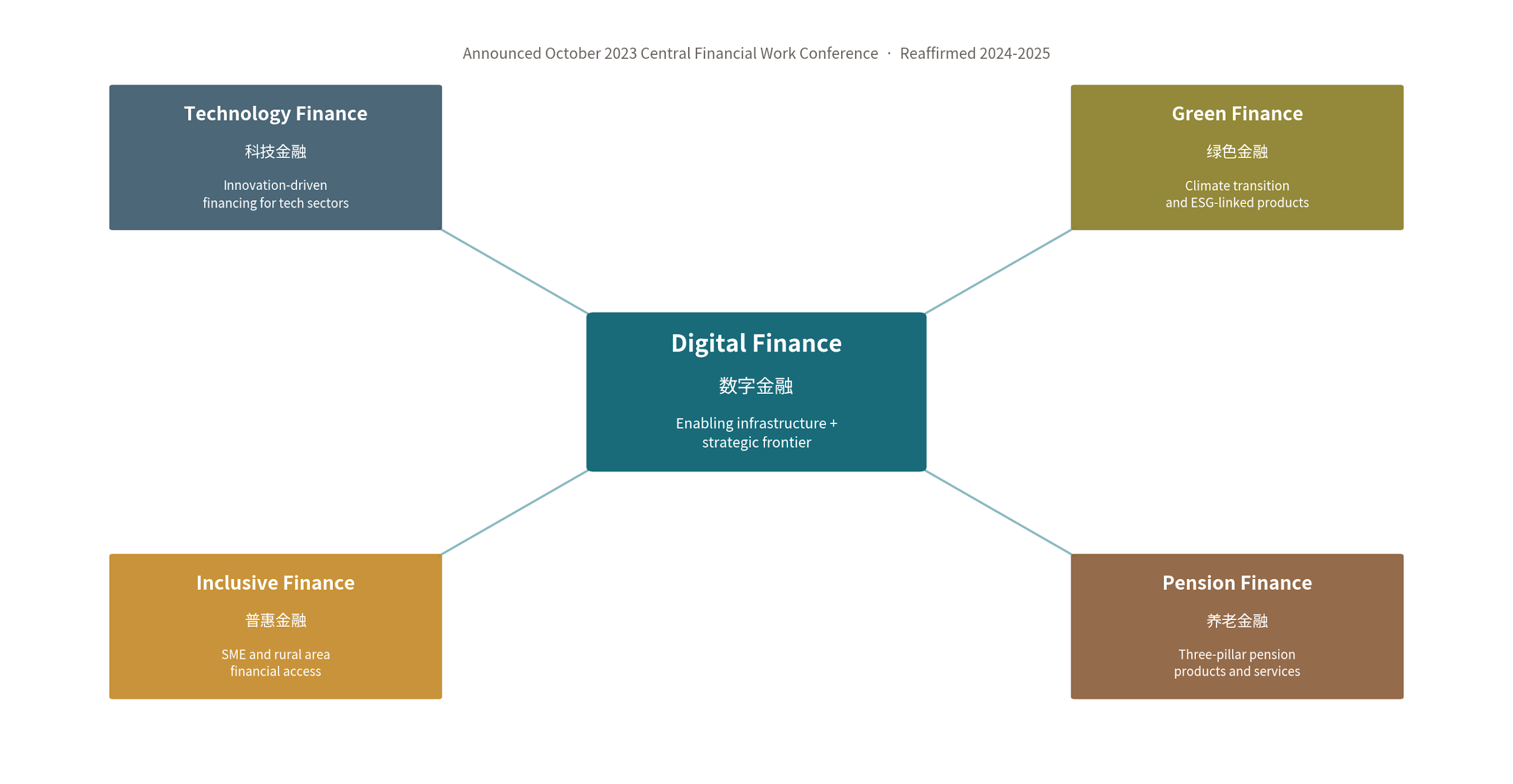

Both threads sit under a broader policy framework, the Five Major Articles of finance, technology finance, green finance, inclusive finance, pension finance, and digital finance, set out by China's financial policymakers as strategic priorities for where the financial system, including its use of technology, should be directed. AI adoption and platform-finance supervision both fall within the technology and digital finance articles of that framework, which is part of why policy treats them as connected rather than separate issues: both are about how far technology is allowed to penetrate financial decision-making, and under what guardrails.

Reading maturity against the framework

The two charts below show AI application maturity across financial functions, then the Five Major Articles framework itself. Read together, they suggest where the next phase of adoption is likely to be permitted to advance fastest: functions and platforms that align cleanly with the stated strategic priorities, inclusive finance, pension finance, and the broader digital finance push, are more likely to see continued regulatory accommodation than functions operating in the regulatory grey areas the platform rectification was originally designed to close.